Many property owners find themselves considering whether or not to move their rental properties to an LLC at some point during their ownership journey. Transferring your rental property to an LLC can protect your personal assets and provide tax flexibility, but it’s not without its drawbacks.

In this article, we’ll explore the pros and cons of moving your rental properties into an LLC so you can make an informed decision based on your financial goals and risk tolerance. Understanding the ins and outs of LLCs will help you make the best decision for you and your properties.

For more information on transferring your rental property to an LLC, reach out to our Good Life Property Management team. We help landlords navigate the best ways to hold title while protecting their investment.

Key Takeaways

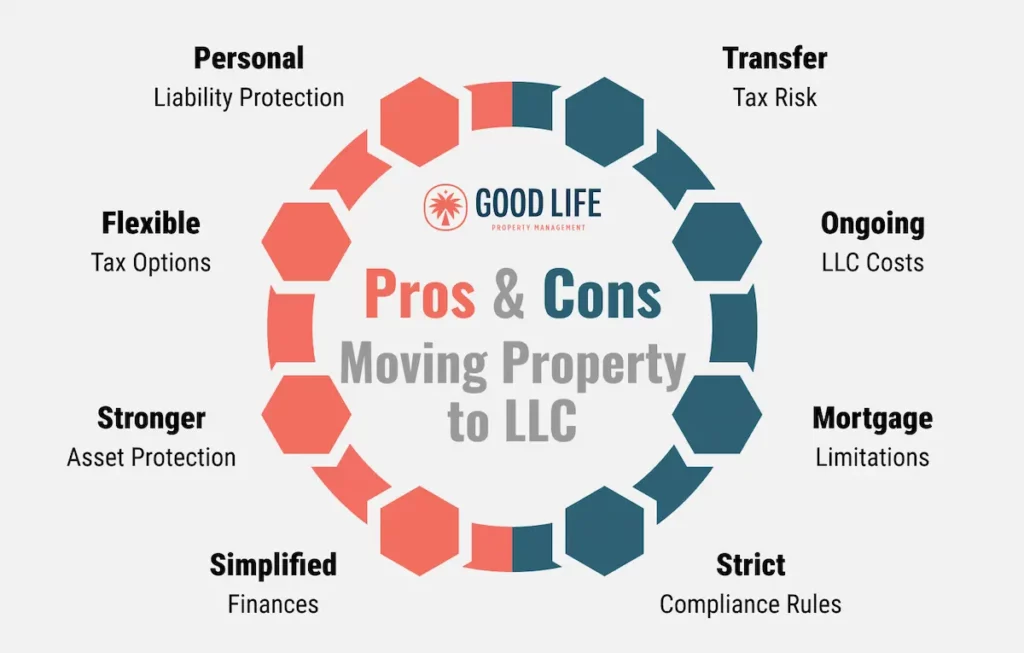

- An LLC protects personal assets but may trigger property tax reassessment and transfer taxes.

- LLCs offer flexible tax options, and easier separation of personal and business finances.

- Setting up and maintaining an LLC can be costly and requires ongoing compliance.

- Transferring a mortgaged property can cause issues with the mortgage provider.

- LLCs work well for property owners who are risk adverse and can take advantage of flexible taxation options.

Table of Contents

What is an LLC?

A Limited Liability Company, or LLC, is a business structure that combines parts of a corporation and a partnership or sole proprietorship. LLCs offer its owners limited liability protection while also giving them more flexible management and taxation options when compared to a traditional corporation.

What Happens When You Form an LLC for a Rental Property?

When you transfer a rental property into an LLC or form an LLC for a rental property, you essentially create a legal separation between your personal assets and your business assets. Think of the LLC as a protective shield for your personal assets. So, if there is ever a lawsuit, injury claim, or other legal action related to your rental property, only the assets held in your LLC are at risk—your personal assets are protected.

When creating an LLC it’s essential that you consult with a lawyer to ensure all of your ts are crossed and your is are dotted. This will help make sure you are compliant with state laws and avoid potential issues like changes to your mortgage terms or reassessment.

Benefits of an LLC for Rental Properties

There are many great reasons to use an LLC for your rental properties. We often recommend LLCs for people with a lot of assets and multiple properties. Let’s take a look at six of the pros of transferring a rental property into an LLC.

1. An LLC can reduce your personal liability

One of the main advantages of holding rental properties in an LLC is the built-in liability protection. As mentioned above, when your property or properties are under an LLC, your personal assets are protected from lawsuits or claims related to those properties. For example, if a tenant sues over an injury that occurs on the property, the lawsuit will be directed at the LLC. Only the assets held within the LLC can be targeted, so your personal assets or any other business assets outside of the LLC are protected.

This protection can give you peace of mind, but it’s important to know that your LLC must maintain proper corporate formalities in order to keep your personal assets protected.

2. There are no real estate excise tax (REET) on transfers

We’re often asked about the potential tax burden that transferring a property can attract, especially if the property has appreciated in value. As California does not have a specific REET, you don’t have to worry about your rental property triggering this additional cost if you transfer it to an LLC.

3. LLCs have flexible tax options

LLCs are extremely flexible when it comes to taxes. If you have a single-member LLC, you report everything on your personal tax return which can make filing much easier come tax time. If there are multiple owners, the LLC is taxed like a team—any profits or losses are shared between the owners and they report it on their taxes.

You can also choose to have your LLC taxed like an S-corporation. If you want to be paid like an employee via a W2 instead of filing in a K1, this is the way to go.

For most small property owners, the best option is the “pass-through” taxation method—this is when income and losses of your business pass through directly to the owners instead of being taxed at the business level. With this method, owners pay tax on their share of the business’s income, at their personal tax rate, which helps to avoid the higher tax rates that come with being a corporation. It’s a popular choice because it can lower overall tax costs for property owners.

4. It offers excellent asset protection

We spoke about how LLCs can protect your personal assets as well as any other business’s assets. Using LLCs is a great way to protect your assets. Ideally, each property you own should have its own LLC in order to create a protective bubble around each property. So, if one LLC faces a lawsuit or debt, the other LLCs—and their associated properties—are protected.

5. You can separate your personal and business finances

Creating an LLC for your property separates personal and business expenses. This will simplify accounting and tax reporting while also making it easier to track your rental income, business deductions, and expenses.

6. LLC are beneficial for estate planning

If you’re planning ahead, an LLC can play an important role in your estate planning strategy. LLCs can streamline ownership and make it easier to bring on new partners, sell a partial interest in the property, or transfer ownership to your heirs. Why and LLC makes this easier is because instead of transferring the property deed, you simply transfer membership interests in the LLC.

Disadvantages of an LLC for Rental Properties

While there are many reasons why LLCs are great for rental properties, there are also some cons to using them. Below, we’ll explore four disadvantages to forming an LLC for your rental properties.

1. Transferring a property can trigger a property tax reassessment and transfer taxes

Transferring a property to an LLC in California can trigger a property tax reassessment. Generally speaking, state law requires a property tax reassessment when a property transfers from one person to another, including when you transfer to an LLC. To avoid a reassessment, the individual transferring the property must own 50% or more of the LLC.

Under California law, cities and counties can impose transfer taxes when property switches hands. Orange County is one of the California counties that has implemented a transfer tax when property title is transferred between a business entity and a person or vice versa. The tax rate is $1.10 per $1,000 of the sale price, but different cities collect additional transfer taxes so it’s important to check with your local tax office beforehand.

2. Setup and ongoing costs

LLCs come with some steep setup costs and ongoing maintenance fees. To file the Articles of Organization with the California Secretary of State, it costs $70, plus an annual minimum franchise tax of $800.

3. It can pose issues with your mortgage

If your property is mortgaged, transferring it into an LLC can create some issues. Standard mortgages often contain a “due on sale” clause that allows lenders to ask for full repayment if the property is transferred to another individual or entity.

This means that transferring your rental property into an LLC could require you to pay off the loan immediately. It’s important to seek legal consultation, but you’ll need to obtain prior approval from the lender to avoid triggering this clause.

4. There are corporate requirements you must maintain

To maintain your LLC’s liability protection, you must keep separate books for the business. You need to keep accurate records of all transactions, income, and expenses related to the property. If you fail to maintain these corporate requirements, you may lose the liability protection an LLC provides.

Is an LLC Right for Your Property?

Deciding whether to transfer your rental properties into an LLC is a very personal choice. It depends on your financial goals, risk tolerance, and personal situation. If protecting your personal assets from lawsuits and having a steady income are important to you, an LLC could be a good choice for you. But if you’re new to property ownership or have a mortgage, the extra costs and dealing with your mortgage provider might not be worth it.

If you do transfer your rental properties into LLCs, make sure you update all of your lease agreements so that they’re between the tenant and LLC.

Manage Your Rental Properties with Good Life

If you’re looking to transfer your rental property to an LLC, working with a property management company can make the process much easier. At Good Life Property Management, we walk you through the paperwork making the process as painless as possible.

At Good Life, we believe life should be enjoyed, not spent sweating the small stuff. That’s why we set out to make property management easy. We care about you, your property, and your tenant. And we do it all so you can Live the Good Life.

Schedule a call to speak with one of our Good Life experts.

LLC for Rental Properties FAQs

Should I put my rental property in an LLC in California?

Putting your rental property into an LLC in California can protect your personal assets but also may trigger a property tax reassessment, so it’s important to weigh the pros and cons for your situation.

What is the best legal entity for a rental property?

The best legal entity for a rental property is typically an LLC, offering liability protection and tax flexibility.

What is the best business structure for multiple rental properties?

For multiple rental properties, an LLC or series LLC is typically the best structure as it provides liability protection and easier management.

Resources and Useful Links:

Steve Welty

Subscribe to Our Orange County Landlord Newsletter

Get in touch with us:

Orange County Property Management Blogs

Should I Allow Pets in My Rental Property?

We’re exploring the pros and cons of a pet-friendly rental property and sharing how to create a pet rental policy that protects you and your property.

The Landlord’s Guide to Emergency Maintenance

Learn how to handle emergency maintenance for your rental. Identify urgent issues, manage after-hours calls, and protect your property.

SB 602 Explained: Protect Your Property from Squatters

Ever wondered why the topic of squatter rights keeps trending in rental property discussions? It seems the idea of someone taking over your vacant property and living there legally for